After the Chinese New Year, although major lead-acid battery enterprises largely resumed normal production, end-use consumption recovered slowly, showing overall weak performance.

During the week, the resumption of production increased among primary and secondary lead enterprises. On the supply side, primary lead smelters that had not yet reached full production by late February are expected to see further output growth, while new capacity for secondary refined lead has entered the raw material stocking phase and is expected to gradually commence production and release output. With ample spot supply in circulation, the discounts for primary and secondary lead have significantly narrowed compared to the first week after the holiday, and are expected to continue discount trading next week.

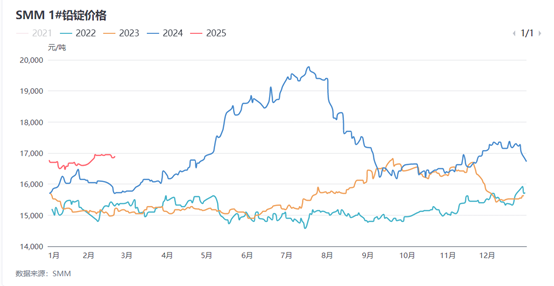

Mid-week, weak spot transactions combined with a widening spread between futures and spot prices. Even after the delivery of the SHFE lead 2502 contract, suppliers remained enthusiastic about transferring to delivery warehouses. Inventories from multiple smelters were shifted to social warehouses, and short-term social inventories of lead ingots are expected to continue building up, putting resistance on lead prices at high levels.

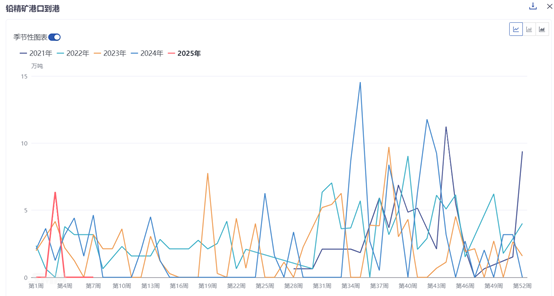

In Q1, supply tightness on the raw material side re-emerged, potentially providing support for lead prices. Regarding lead concentrates, the 2025 long-term contract TC quotes for imported ores are expected to decline YoY compared to 2024, with TC quotes for silver-bearing lead concentrates likely to show more pronounced pricing adjustments. This week, a mine trader told SMM that the recent supply deficit of lead concentrates has not improved, with almost no USD quotes available in the market, and trade in concentrates is primarily conducted in RMB minus adjustments.

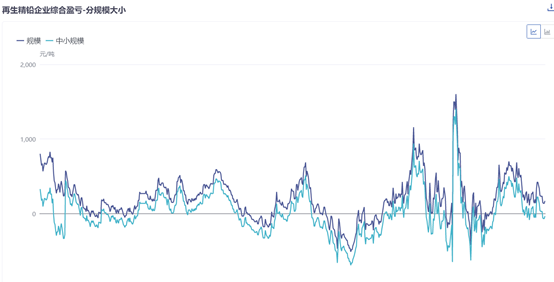

Additionally, the limited supply of scrap batteries has begun to constrain the profit margins of secondary lead, and under the condition of ample refined lead supply, the discount for secondary lead has not widened in tandem with primary lead. In some regions, secondary refined lead has even seen inverted pricing. Fundamentals side, although inventory buildup pressure has weakened lead price movements, raw material support has become more prominent again. In the short term, lead prices are expected to continue fluctuating at high levels, and attention should be paid to whether improvements in downstream consumption can drive lead prices out of the fluctuation range.